2026-06-06 — views Intermediate

A quarterly options-hedging calendar — the H2 2026 risk cadence

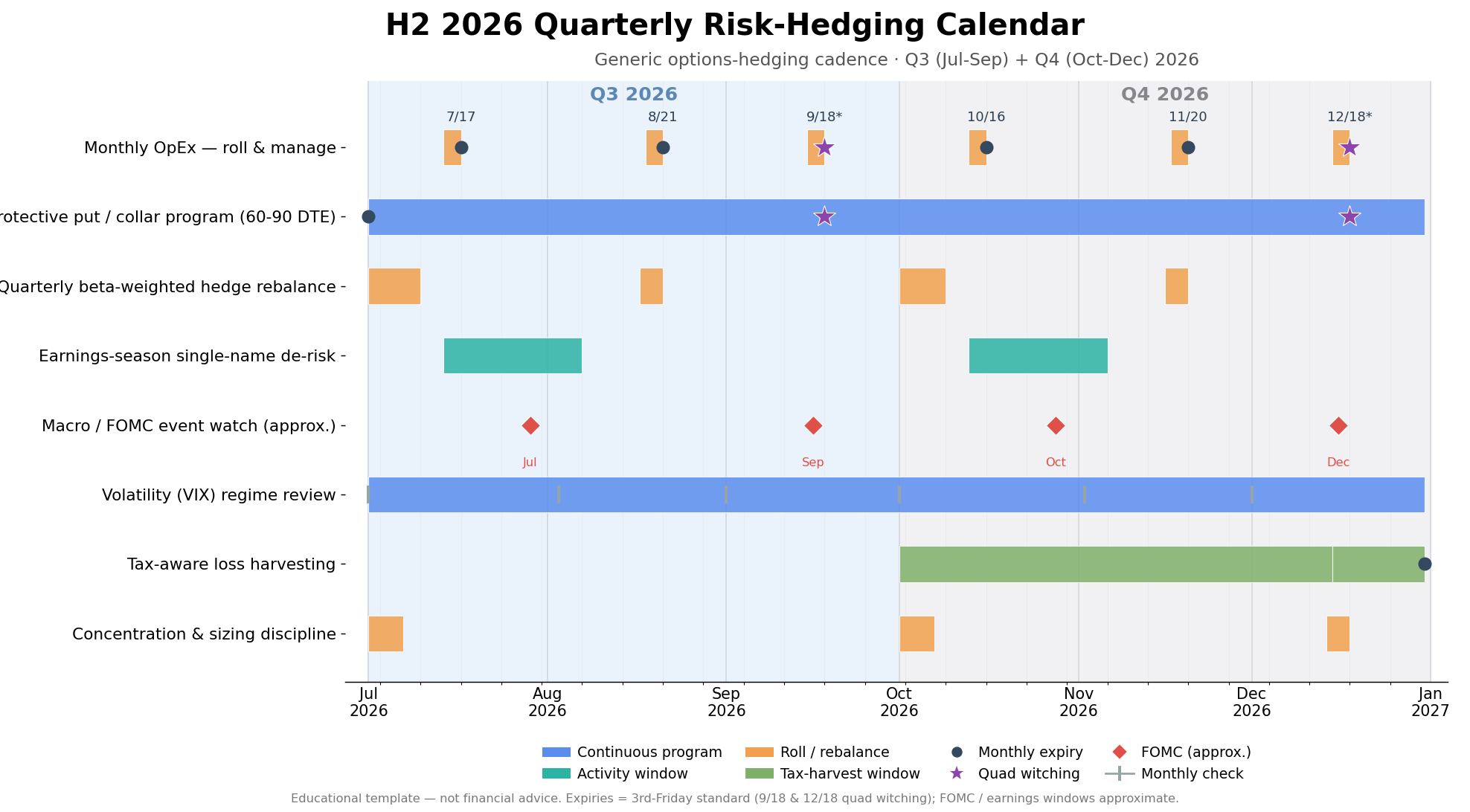

A generic, repeatable options-hedging calendar for H2 2026: monthly expiries & quad witching, earnings de-risk windows, FOMC dates, a standing put/collar program, VIX regime checks, and year-end tax-loss harvesting. Education, not financial advice.

A hedging program rarely fails because the hedge was wrong — it fails because it was done ad-hoc, reacting after the drawdown instead of on a schedule. A calendar turns risk management into a repeatable cadence: the same checks, on the same dates, every quarter. Below is a generic options-hedging calendar for the second half of 2026 (Q3 + Q4), built around the events that actually move a book — monthly expirations, earnings seasons, FOMC decisions, and year-end tax work. It builds on Options 101 and risk & leverage. Education only, not financial advice.

H2 2026 hedging cadence — eight workstreams across Q3 (Jul–Sep) and Q4 (Oct–Dec). Generic template.

The eight workstreams

| Workstream | Cadence | Purpose |

|---|---|---|

| Monthly OpEx — roll & manage | Each 3rd-Friday expiry | Roll or close expiring hedges; avoid pin & assignment surprises |

| Protective put / collar program | Continuous, 60–90 DTE | A standing downside floor; re-strike each quarter |

| Quarterly β-weighted rebalance | Quarter start + mid-quarter | Re-size hedges to current portfolio beta and notional |

| Earnings-season de-risk | Mid-Jul–early-Aug; mid-Oct–early-Nov | Trim or hedge single-name event risk before prints |

| Macro / FOMC watch | 4 Fed meetings in H2 | Pre-position for rate-decision volatility |

| Volatility (VIX) regime review | Monthly | Buy protection when vol is cheap; harvest when it is rich |

| Tax-aware loss harvesting | Oct – mid-Dec + year-end | Realize losses, manage wash sales, net gains and losses |

| Concentration & sizing discipline | Quarter start + year-end | Trim oversized positions back to your limits |

Key H2 2026 dates

| Date | Event |

|---|---|

| Jul 17 | Monthly expiry |

| ~Jul 28–29 | FOMC (approx.) |

| Aug 21 | Monthly expiry |

| ~Sep 15–16 | FOMC (approx.) |

| Sep 18 | Quad witching (quarterly) |

| Oct 16 | Monthly expiry |

| ~Oct 27–28 | FOMC (approx.) |

| Nov 20 | Monthly expiry |

| ~Dec 15–16 | FOMC (approx.) |

| Dec 18 | Quad witching (quarterly) |

| Oct 1 – Dec 15 | Tax-loss harvesting window |

How to use it

- Pick the lanes that fit your book. A long-only equity holder leans on the put/collar program and earnings de-risk; a premium seller leans on OpEx management and VIX timing.

- The value is the cadence, not the precise dates. Even approximate timing beats reacting after a drawdown — the calendar removes the discretion that losses exploit.

- Pair it with hard limits. Combine the schedule with a fixed risk budget per position (see risk & leverage).

- Confirm the live dates. Verify FOMC dates against the Fed calendar and earnings against each issuer’s IR page before acting.

Assumptions & limitations

- Generic template — not tied to any portfolio, holdings, or risk tolerance.

- Expiries use the standard US monthly 3rd-Friday; Sep 18 & Dec 18 are quarterly quad-witching dates.

- FOMC and earnings windows are approximate — confirm against the Federal Reserve calendar and issuer IR.

- Not financial advice. A calendar organizes when you review risk; it does not tell you which hedge to put on.

The under-considered angle

Cadence beats cleverness. Most blow-ups don’t come from choosing the wrong hedge — they come from skipping the boring schedule: the protection that was never rolled, the earnings event that wasn’t trimmed, the concentrated position that was never cut back. A calendar’s real job is to remove discretion at exactly the moments — right before a catalyst, deep in a drawdown — when discretion is most likely to fail you.

Educational template — not financial advice. Dates are illustrative; confirm against official sources.